.svg)

June 2, 2026 - Disseminated On Behalf Of Strathmore Plus Uranium Corp

Bull case. Bear case. Ten reasons to look at Strathmore Plus Uranium right now. Plus a complete narrative walkthrough of every major press release from the start. This is the long read.

Bottom Line · The 60-Second Version

When President Trump signed the executive order in March of 2025 designating uranium a critical mineral, most people on Main Street did not notice. Wall Street did. Cameco, the world's second-largest uranium producer, was trading around $40 a few years ago. It now changes hands above $107, up roughly 360% over three years and another 26% year-to-date in 2026 alone. Uranium Energy Corp has gone from under $4 to north of $15. NexGen, Denison, Energy Fuels: almost the entire uranium complex has been repriced as the policy backdrop, the AI-driven power crunch, and a structural supply deficit have converged into the most bullish setup the sector has seen in two decades.

The story is no longer controversial. It is a top-down political mandate. In May of last year the White House issued a second executive order, this one specifically aimed at "reinvigorating the nuclear industrial base," meaning mine it, process it, refine it, all on American soil. In January 2026 the administration invoked Section 232 trade authority against imported processed critical minerals, including uranium. The United States currently imports roughly 95% of the uranium it consumes. The administration has decided that is a national security problem and is throwing the full weight of the Defense Production Act, federal land prioritization, and accelerated permitting at fixing it.

What has not been fully repriced yet, in our view, is the front end of the funnel: the early-stage explorers who actually own the dirt and the drill collars that the producers will eventually need. The producers have already moved. The drill-bit-stage juniors, in many cases, have not. That gap is the trade.

This is where Strathmore Plus Uranium Corporation (CSE: SUU / OTCQB: SUUFF / FSE: TO3), ticker $SUU, enters the conversation. And this is not a new story. It is the latest chapter of one.

The producers have already been repriced. The early-stage explorers have not. That gap is the trade.

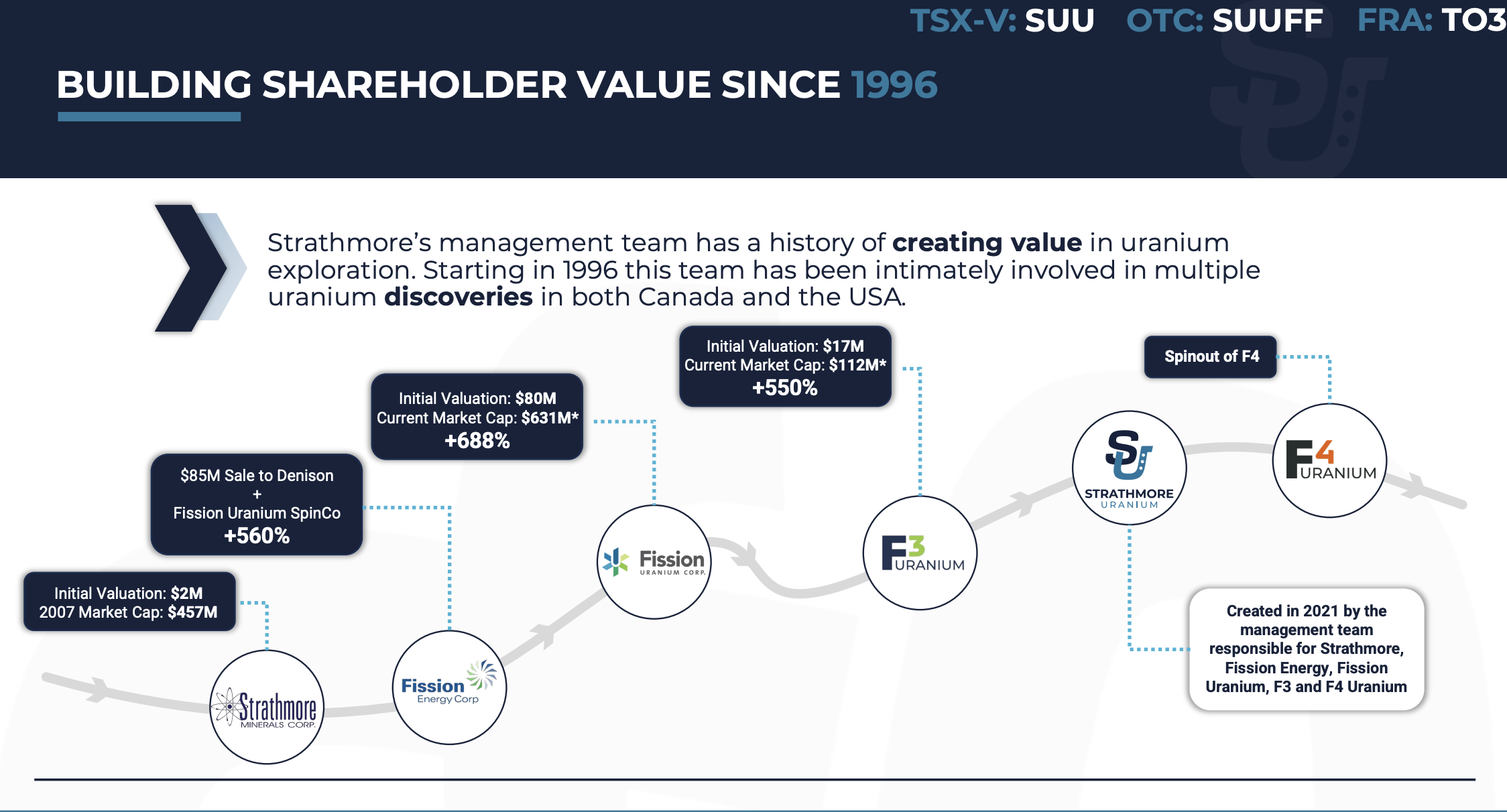

The management team behind Strathmore has built and sold four prior uranium companies since 1996. Strathmore Minerals went from a $2 million startup valuation to a $457 million peak market cap. Fission Energy generated a documented return of more than 560% on the way to its $85 million sale to Denison plus a SpinCo. Fission Uranium ran from an $80 million initial valuation to a $631 million market cap, a 688% gain. F3 Uranium delivered another 550%. F4 Uranium was spun out in 2021. Now the same group is running the playbook a fifth time, on American soil, inside the most uranium-friendly U.S. administration in fifty years.

The current vehicle, by comparison, trades at roughly $14 million. That is the setup. Below, the bull case, the bear case, the ten reasons, and a complete narrative walk through every press release that brought us here.

The Bull Case

The bull case for Strathmore is, in our view, the cleanest in the U.S. uranium exploration space right now, and it does not depend on the price of uranium going to $200 a pound. It depends on three things being true at the same time, and all three currently are.

Uranium is now formally designated a critical mineral under the March 2025 executive order. Federal lands are being prioritized for mining over essentially every other use. Permitting is being accelerated under the FAST Act. The Defense Production Act has been invoked. And the United States is openly negotiating tariffs and supply agreements aimed at choking off Russian and Kazakh imports.

For a Wyoming-based ISR-amenable uranium explorer, this is not a tailwind. It is a jet engine.

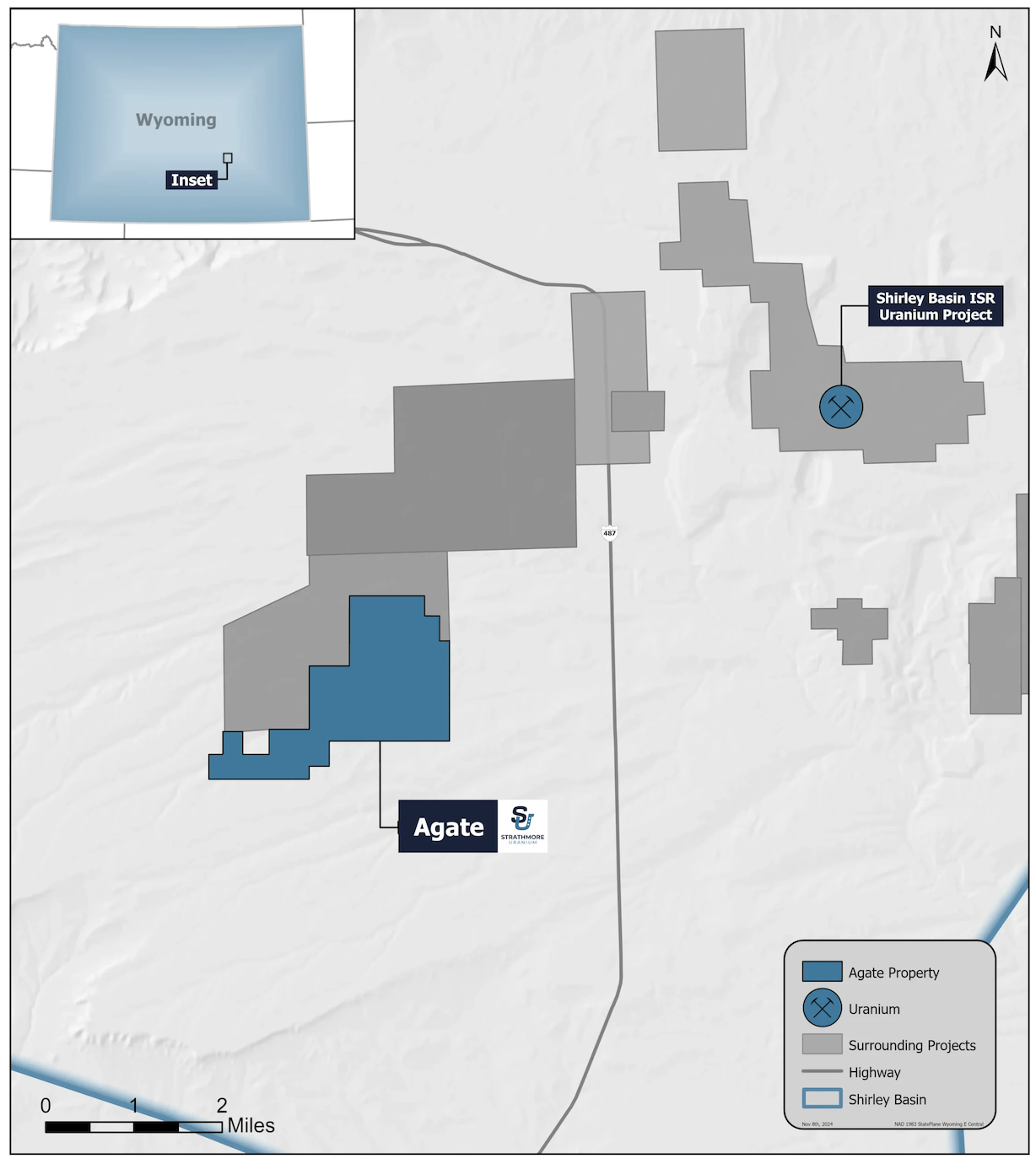

The state of Wyoming itself is one of the most pro-mining jurisdictions on Earth. Drilling costs in Wyoming are a fraction of what they are in the Athabasca Basin in Canada. Roughly 90% of all U.S. uranium produced in 2018 came from Wyoming. The Shirley Basin, where Strathmore's flagship Agate project sits, hosted the first commercial in-situ recovery mine in the United States. Roughly 53 million pounds of uranium have been mined out of that basin historically. None of this is theoretical. It has been done before, on the same ground.

You do not have to bet on uranium policy improving. It already has improved. The question is which companies have the right asset, in the right jurisdiction, with the right management, to be repriced as that policy reality keeps landing.

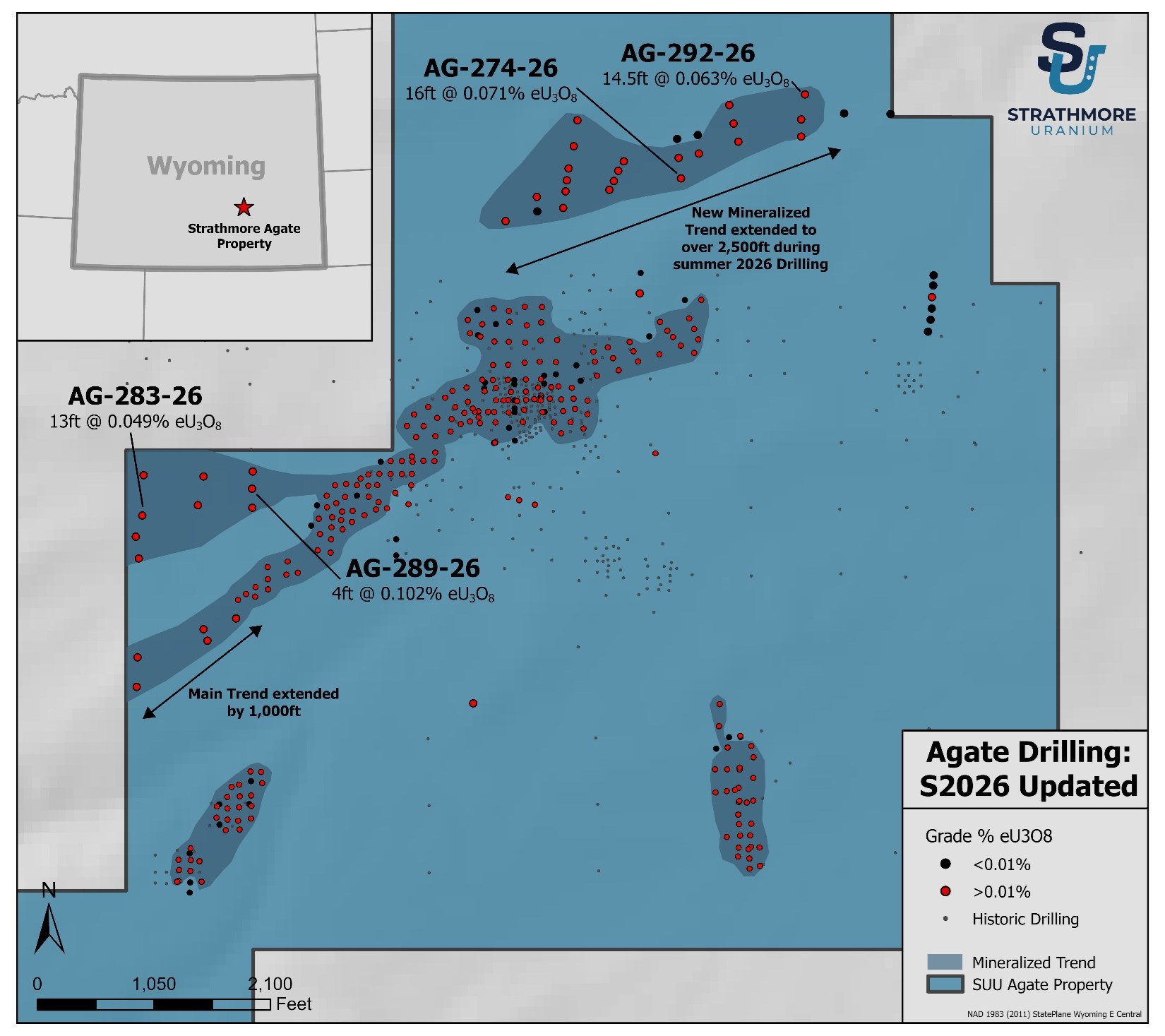

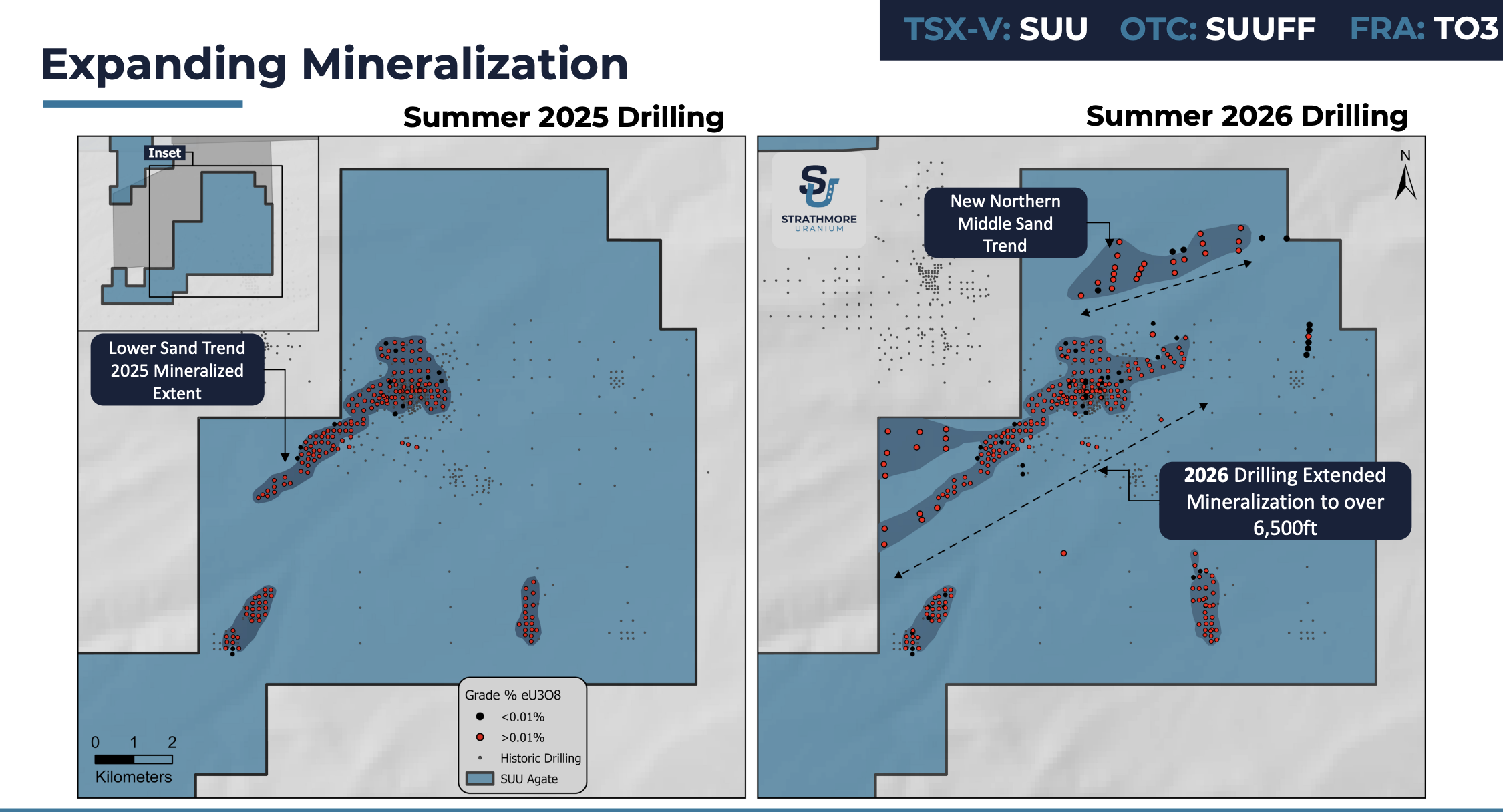

Agate is 124 wholly owned lode mining claims covering roughly 2,560 acres of ground that Kerr-McGee, at the time the largest uranium miner in the United States, drilled extensively in the 1970s. Strathmore has now completed 294 drill holes of its own across the property, and on May 20, 2026 confirmed that over 85% of those holes have hit uranium mineralization.

An 85% hit rate is an extraordinarily high number by any standard in junior uranium exploration. It does not, in itself, guarantee an economic deposit, but it tells you the geological model is working, the targeting is good, and the company is drilling into a real, contiguous roll-front system.

The mineralization at Agate sits between 20 and 150 feet deep, much of it below the water table. That depth profile, combined with the host rock (the Eocene Wind River Formation, an arkosic-rich sandstone), is the textbook setup for in-situ recovery (ISR), the cheapest and lowest-impact uranium extraction method currently used in North America. ISR is also the permitting path Wyoming is most experienced with, which matters enormously for timelines.

And here is the part that should jump off the page for any uranium investor: $SUU's Agate Project sits directly adjacent to projects held by Cameco and UEC, and lies near UR-Energy's satellite ISR mine that began production in April 2026. The largest names in U.S. uranium have already staked, drilled, and started producing on the same ground. The market has validated the district with billions of dollars of capital. Strathmore now has the chance to grow a resource estimate inside that same fairway.

This is the part of the bull case that, frankly, gets underweighted by most investors looking at junior miners. CEO Dev Randhawa and the broader Strathmore management group have a documented thirty-year track record of going into uranium districts, drilling, proving deposits, and monetizing them, whether through outright sales, spinouts, or strategic transactions.

The receipts, again:

Past performance is not a guarantee of future results, and we will say that more than once in this article. But pattern recognition matters in junior mining. Investors who backed prior Randhawa-led uranium vehicles at the explorer stage and held through the discovery cycle have, in several cases, been rewarded handsomely. Whether this iteration delivers a similar outcome is unknown. The setup, however, is unusually consistent with what worked before.

Same management. Same playbook. Same uranium thesis. Different decade. Different jurisdiction. Same shot at a multi-bagger outcome, with the caveat that no such outcome is ever guaranteed.

Critical mineral designation. The most pro-uranium U.S. administration in a generation. A Wyoming property with an 85% drill hit rate, sitting next door to Cameco and UEC ground. A maiden resource estimate in the company's stated near-term plan. Three permitted projects. And a management team that has demonstrably created wealth from this exact playbook four times before. $SUU's market cap is roughly $14 million.

The peer-set developers in the same Wyoming exploration space trade between $700 million and $6.7 billion. We are not predicting Strathmore closes that gap. We are observing that the math, if even partially closed by a successful resource definition program, is asymmetric. That is the bull case in a sentence.

The Bear Case

No article about a small-cap uranium explorer is worth reading if it skips this section. $SUU is a junior exploration company. Junior exploration companies are inherently speculative. There are several legitimate reasons to be cautious, and we want to lay them out plainly.

Strathmore has no current revenue, no producing asset, and no NI 43-101 resource estimate yet. It is an exploration-stage company. That means the company depends on capital markets to fund its drilling and operations, and in junior mining, that typically means dilution.

Strathmore has closed multiple private placements over the past two years, including a $1.1 million raise in March 2026, a $665,000 raise in mid-2025, and a $1.4 million raise in early 2024. None of these are large by industry standards, and management has so far kept the share count tight, but investors should expect continued financings, particularly as drilling activity scales, and should size positions accordingly. Dilution is a structural risk for every junior, and Strathmore is no exception.

The uranium spot price, while currently strong near $84 per pound, is volatile and has historically been brutal on junior explorers when it turns. Uranium fell from $62 per pound in 2011 to $35 by 2020 in the aftermath of the Fukushima disaster. Spot prices could fall again on a major nuclear incident, on Kazakh oversupply, on a global recession that softens electricity demand, or simply on profit-taking by speculative funds.

Strathmore's equity, like all uranium juniors, is highly sensitive to spot. If the broader uranium thesis breaks, this stock will break with it, and small caps typically draw down further than the producers when sentiment shifts.

An 85% hit rate is impressive. It is not, in itself, an NI 43-101 compliant resource. Drill assays are not pounds in the ground. A high hit rate does not guarantee that the grades and thicknesses ultimately delineated will support an economic ISR operation. Until a maiden resource is published and economic studies are completed, there is genuine uncertainty about what Strathmore actually owns in pounds-in-the-ground terms.

Even after a resource is published, moving to production requires a Plan of Operation submittal (which the company has indicated it is preparing), federal and state permitting, and capital that the company does not currently have on its balance sheet. Timelines for federal mining permits in the United States, even under an accelerated regime, are measured in years, not months.

Strathmore trades on the CSE in Canada and OTCQB in the United States. Daily volume is modest. Bid-ask spreads can be wide. This is not a name you can move a large position in or out of without affecting price. For some investors, the illiquidity is precisely the source of the asymmetric setup; for others, it is a disqualifying feature.

The bull case rests partly on management's track record. Past performance is not, and we want to be emphatic about this, a reliable indicator of future results. The team behind Strathmore Minerals, Fission Energy, Fission Uranium, F3 and F4 has a real history of value creation in uranium. That history was created under specific market conditions and on specific assets that are different from the current Wyoming portfolio. The outcome here may be similar. It may be better. It may be worse. Investors who project a guaranteed repeat are not being careful.

The bull case still wins on our read of the evidence, but it wins on probabilities, not certainties. Anyone telling you a junior uranium stock is "going to" do anything is selling you something. Size positions accordingly.

The Core of the Trade

Below, the ten points we think capture why Strathmore Plus Uranium deserves a place on a serious uranium watchlist right now, written in roughly the order we think about them. Some of these will sound familiar by now. That is intentional. The repetition is the message.

Reason · The Team

Strathmore Minerals reached a $457 million peak market cap. Fission Energy delivered a 560% return en route to its $85 million Denison sale and SpinCo. Fission Uranium ran 688% to a $631 million market cap. F3 Uranium added another 550%. The team running $SUU today is the same team that built all four. Pattern recognition in junior mining is not destiny, but it is not nothing, either. When the same group lines up at the same plate for the fifth time, you at least pay attention.

Reason · Policy

Trump's March 2025 executive order formally designated uranium a critical mineral. The May 2025 nuclear EO followed. The January 2026 Section 232 action targets imported processed uranium. The federal government is invoking the Defense Production Act on behalf of U.S. uranium producers. There is no recent precedent for a policy stack this aggressive in favor of domestic uranium. If you wanted Washington to design a tailwind for a Wyoming-based ISR uranium explorer, it would look almost exactly like this.

Reason · Drill Results

Across 294 holes drilled at the Agate Project to date, over 85% have intersected uranium mineralization, confirmed in the company's May 20, 2026 press release. That is among the highest hit rates we have seen disclosed by a junior uranium explorer in North America. It does not yet equate to an NI 43-101 resource. It does suggest the geological model is working, the targeting is sound, and the company is drilling into a real, contiguous roll-front system.

Reason · The Neighbors

$SUU's Agate property sits directly adjacent to projects held by Cameco and UEC, and lies near UR-Energy's satellite ISR mine that began operations on April 23, 2026. When the largest names in the U.S. uranium space stake ground next to yours, drill it, and bring it into production, it is both a market validation of the district and a road map for what an ultimate exit could look like.

Reason · The District

This is not frontier exploration. The Shirley Basin has historically produced 53 million pounds of uranium, including from the first commercial in-situ recovery operation in U.S. history during the 1960s. Strathmore is exploring inside a proven district that Kerr-McGee, at the time the largest uranium miner in the United States, drilled extensively in the 1970s. The geological homework was effectively done decades ago.

Reason · The Method

Uranium at Agate sits between 20 and 150 feet below surface, much of it below the water table. That depth profile, combined with the host rock, is the textbook setup for in-situ recovery, the cheapest, lowest-impact uranium extraction method currently used in North America. The company has stated it is now advancing toward submitting a Plan of Operation with the U.S. Bureau of Land Management and the Wyoming Department of Environmental Quality.

Reason · The Valuation

According to data drawn from the company's most recent corporate presentation: $SUU traded at roughly $14 million, while peer developers in the same Wyoming uranium exploration space traded between $700 million and $6.7 billion. UEC alone is north of $6.4 billion in enterprise value. Energy Fuels is over $6.7 billion. This is not a prediction that $SUU will reach those valuations. It is simply an observation that the math, if even partially closed by a successful resource definition program, is asymmetric.

Reason · The Catalyst Path

Strathmore management has indicated, in the May 20, 2026 release, that it plans to "continue to drill and expand the mineralization and generate a resource estimate once sufficient drill hole information allows." A maiden NI 43-101 resource is, historically, one of the most significant re-rating catalysts a junior explorer can deliver. We do not have a published timeline. We do have an explicit company statement of intent.

Reason · The Portfolio

$SUU is not a one-asset story. Beyond Agate, the company holds the Beaver Rim property (265 lode claims, 5,475 acres, with stacked roll fronts confirmed in late 2024) and the Night Owl project (a former producing surface mine that operated in the early 1960s). All three are permitted for drilling. That diversification across multiple Wyoming districts reduces single-asset risk and gives management optionality on where to put exploration capital next.

Reason · The Window

Cameco is up roughly 360% in three years. UEC is selling pounds at $101 per pound on unhedged contracts. Uranium spot is trading near $84 with Citi forecasting a path to $100 to $125 this year. The producers have already been repriced. The early-stage explorers have not. That gap is the trade. Whether it closes, and whether $SUU is the right vehicle to play it, is for each investor to decide. We think it warrants the homework.

The Confirming Data Point

If you wanted a real-world validation of the district economics around $SUU's flagship Agate property, you could hardly do better than an actual uranium producer building an actual processing plant on the same ground, on a timeline measured in months rather than years. That is precisely what is happening. UR-Energy's Shirley Basin plant sits 5.3 miles east of Agate, and the company has said it is advancing toward commencement of operations and ramp-up of production in 2026 (company disclosures, January 2026 site update).

Consider what that means for $SUU shareholders. A licensed, NRC-approved, NI 43-101-defined uranium producer is bringing a processing facility into commercial operation next door, on the exact same Wyoming roll-front geology, in the same Shirley Basin sandstone aquifer system, using the same in-situ recovery method that Agate's depth profile and host rock are textbook-suited for. That single fact validates the district economics, de-risks ISR on Agate's specific ground, compresses the conceptual permitting path, and puts an active, producing operator on the doorstep, a meaningful corporate-development signal in its own right.

The market has not been treating Agate as if a producing uranium mine is being commissioned this year on the property next to it. That gap between perception and on-the-ground reality is, in our view, one of the most interesting setups in the U.S. uranium junior space right now.

Consistent Execution

One of the cleanest ways to evaluate a junior explorer is to look at what their drill bit has actually done to the size of their deposit, year by year. Promotion is cheap. Drill program after drill program of extended mineralization is not.

By that measure, $SUU's record is unusual. Every annual drilling campaign since the program began at Agate in October 2023 has materially expanded the mineralized footprint, and the 2026 program added an entirely new horizon on top of that. Here is the year-by-year progression:

Strathmore commences drilling at Agate in October. The first 800-foot step-out hole hits. The mineralized zone is more than doubled within the first six weeks of drilling. By November, the company reports uranium mineralization in 93% of holes drilled.

93% hit rate · First roll-fronts confirmed

University of Wyoming geophysics pinpoints new roll-front targets at Agate. Strathmore secures a permit for a 200-hole drilling program. In July, the Agate mineralized trend is tripled in length. A one-mile step-out hits favorable grades and thickness. By December, the company reports stacked roll fronts at Beaver Rim, a second prospective project in the portfolio.

Trend tripled · 1-mile step-out hits · Beaver Rim: stacked roll fronts

Strathmore lists on the CSE. The 2025 drill program extends Agate mineralization by another 1,200 feet in August, then extends the southern trend to over 1,300 feet in September. By the end of the season, the total mineralized footprint at Agate stretches to over 5,200 feet. Closing the year, the company strategically stakes additional claims.

+1,200 ft (Agate) · Southern trend: 1,300+ ft · Total footprint: 5,200+ ft

The Spring 2026 program drills 48 holes at an 81% hit rate. The Lower Sand trend extends an additional 1,000 feet westward, to nearly 6,000 feet of total length. An entirely new Middle Sand trend is identified over 2,500 feet, stacked above the Lower Sand. By May 20, Strathmore confirms an 85% mineralization hit rate across all 294 holes drilled since 2023. The company moves toward filing a Plan of Operation with BLM and Wyoming DEQ. A maiden NI 43-101 resource estimate is now an explicit company milestone.

Lower Sand: ~6,000 ft · Middle Sand: new, 2,500 ft · Project-wide: 85% hit rate · Resource estimate targeted

The pattern is the point. Every year, the asset gets bigger. Every year, the hit rate stays in the 80 to 90 percent range. Every year, new mineralized geology is identified inside the property boundary. $SUU has not delivered a single quiet drill season since the Agate program started, and the 2026 numbers are bigger than the 2025 numbers, which were bigger than 2024, which were bigger than 2023.

In junior uranium, that kind of compounding consistency is rare. It is also exactly the pattern that, historically, has preceded major resource-definition catalysts in the prior management-led vehicles (Strathmore Minerals, Fission Energy, Fission Uranium, F3 Uranium) that this same team has built.

Every annual drill program has added to the deposit. 2026 was not a re-drill of 2025. It found an entirely new horizon stacked on top of last year's footprint.

The Receipts · Deep Dive

This is the part of the article you should not skip. A junior uranium story is told one press release at a time, and the pattern of consistent, drill-bit-driven progress is more important than any single number. What follows is a chronological walk through the press release trail that brought $SUU from the start of its Agate program in October 2023 to a company drilling 294 holes with an 85% hit rate adjacent to Cameco and UEC.

We have stripped this down to the nine releases that actually moved the story. Read top to bottom for the full arc.

October 11, 2023 · The Starting Line

Strathmore Commences Drilling at Agate PropertyThe Agate drill program, the one that would ultimately produce the 85% hit rate now in 2026, formally begins. Every subsequent $SUU press release ladders back to this moment.

Why it matters: the starting line of the story that the rest of this article is about. Every subsequent Agate release builds on this one.

November 16, 2023 · The Establishing Moment

Strathmore Hits Uranium Mineralization on 93% of Holes DrilledThe single most important release of the early $SUU story. A 93% mineralization hit rate across the early Agate drilling. This is the number that established Strathmore as a serious uranium discovery story rather than a routine junior, and it set the benchmark every subsequent program would be measured against.

Why it matters: the hit rate is the headline number that every subsequent $SUU communication has had to live up to. As of May 2026, with a much larger sample of 294 holes, the rate has settled at 85%, still extraordinary for the U.S. uranium space.

February 20, 2024 · Academic Validation

University of Wyoming Break-Through Geophysics Pinpoints Roll Front Targets at AgateThe University of Wyoming Geophysical Grant Study identifies new roll-front targets at Agate using magnetics and gravity studies. Independent academic validation of the geological model, and a road map for where to drill next.

Why it matters: free, university-grade exploration intelligence. The kind of partnership most juniors cannot get. The May 2026 PR confirms that subsequent drilling validated UW's predictions. The academic targeting works in the field.

July 9, 2024 · The Deposit Triples

Strathmore Triples Length of Mineralized Trend at AgateThe Agate mineralized trend is tripled in length. Step-by-step extension is exactly how Fission Uranium's PLS deposit grew from initial discovery into one of the largest high-grade uranium discoveries in modern history. The pattern is replicable.

Why it matters: resource expansion in real time. Every multiple makes the eventual maiden NI 43-101 resource bigger. This is the moment the deposit started looking material rather than just promising.

December 3, 2024 · Project #2 Comes Alive

Strathmore Hits Mineralization with Stacked Roll Fronts at Beaver RimThe first Beaver Rim drill results come in. Stacked roll fronts, a particularly attractive geological feature, because they mean multiple horizons of mineralization in the same vertical column. $SUU is no longer a one-asset story.

Why it matters: Beaver Rim is not just a land bank. It is a real second uranium project. Stacked roll fronts are the kind of geology that supports significant ISR resource bases, and the geology that produced Wyoming's largest historical mines.

May 8, 2025 · Institutional Step-Up

Strathmore Announces CSE ListingThe move from TSX-V to the CSE, generally a positive signal for junior miners seeking better trading access and lower listing friction. $SUU now trades as CSE: SUU on the Canadian Securities Exchange, alongside its OTCQB: SUUFF listing in the United States.

Why it matters: cleaner trading vehicle, broader investor access. Many of the most successful North American junior uranium names trade on the CSE for exactly these reasons.

August 20, 2025 · The Mineralization Keeps Growing

Strathmore Increases Uranium Mineralization at Agate by 1,200 FeetMineralization at Agate is extended by another 1,200 feet. The mineralized footprint just keeps growing, drill program after drill program. This is what consistent execution looks like in junior uranium.

Why it matters: every footstep extension is a future pound in the future resource estimate. This is how juniors build a resource, one drill program at a time. $SUU has done it without a single quiet quarter.

May 5, 2026 · Inflection Point ★ Flagship Release

Strathmore Hits 81% Mineralization Rate and Advances Agate Expansion, New Middle Sand Trend Confirmed Over 2,500 FeetA massive release. 48 holes drilled this spring. 81% hit rate. A brand-new Middle Sand mineralized trend identified over 2,500 feet. The Lower Sand trend extended westward by 1,000 feet (now nearly 6,000 feet in total length). Highlight intercepts include AG-274-26 at 16.0 ft at 0.071% eU3O8 and AG-289-26 at 4.0 ft at 0.102% eU3O8. And critically: the company announced it would advance toward filing a Plan of Operation with the U.S. Bureau of Land Management and the Wyoming Department of Environmental Quality.

Why it matters: this is the release that materially changed the size of the prize at Agate. A second mineralized horizon (Middle Sand) means $SUU is now potentially looking at stacked ISR-amenable mineralization, just like at Beaver Rim. And the Plan of Operation announcement is the first formal step toward production permitting.

May 20, 2026 · The Capstone ★ Flagship Release

Strathmore Confirms 85% Mineralization Hit Rate at AgateThe capstone release. Across all 294 holes drilled at Agate since 2023, mineralization is present in over 85% of holes. Chemical assays from 20 core samples confirm the presence of uranium across multiple intervals, including AG-244-25 at 0.1250% U3O8 (chemical assay) and AG-245-25 at 0.0397% U3O8. $SUU management explicitly states it plans to "continue to drill and expand the mineralization and generate a resource estimate once sufficient drill hole information allows."

Why it matters: this is the release the whole story has been pointing toward. The hit rate is now a confirmed, project-wide, multi-year number, not a single program's noise. And the company has, for the first time, explicitly signaled a maiden resource estimate as the next major milestone. That is the catalyst the market will be watching for.

The Catalyst Calendar

2026 · Highest priority

The flagship continues. The company has disclosed plans for a ~100-hole drill program at Agate targeting another 15,000 feet of drilling. This is the program that will most directly determine the size and grade of the eventual maiden resource estimate. Planned workstream: extending mineralization intersected in 2023 to 2025, plus a dedicated core study with XRF and chemical assay analysis, plus additional claim staking. Status as of Feb 2026 deck: Planned.

2026 · High priority

After confirming stacked roll fronts at Beaver Rim in late 2024, the company has scheduled a 6,000 to 10,000 ft drill program covering 5 to 10 holes in 2026. The goal: identify the full mineralized trends inside the project claims and prepare the asset for its own resource definition path. Status as of Feb 2026 deck: Planned.

2026 · Setup phase

At the historic Night Owl project, a former producing surface mine that operated in the early 1960s, Strathmore is doing the targeting work that comes before drilling. The goal is to identify a geophysical footprint to help in future drill targeting. Planned workstream: geophysical and surveying. Status as of Feb 2026 deck: Planned.

Explicitly targeted

In the May 20, 2026 press release, Strathmore explicitly stated it plans to "continue to drill and expand the mineralization and generate a resource estimate once sufficient drill hole information allows." A maiden resource is historically one of the single most significant re-rating catalysts a junior explorer can deliver. A specific date has not been published, but the stated intent is on the public record.

In progress

In the May 5, 2026 release, Strathmore announced it will advance permitting the project with the completion and submittal of a Plan of Operation with the U.S. Bureau of Land Management and the Wyoming Department of Environmental Quality. This is the first formal regulatory step on the path toward eventual ISR production.

2026 · External catalyst

Independent of $SUU's own news flow, UR-Energy's Shirley Basin processing plant, 5.3 miles east of Agate, is on track for production ramp-up in 2026. Every milestone UR-Energy announces effectively validates the district economics on $SUU's ground by extension.

Inside the next twelve months, an investor in $SUU is looking at: a ~100-hole flagship drill program, a 5 to 10 hole second-asset drill program, geophysical work on a third asset, the path to a maiden resource estimate, an active permitting application with two regulators, and a producing uranium plant being commissioned 5.3 miles east. That is a deep catalyst calendar for a $14 million market cap.

The Full Trail

For investors who want the complete chronological scan in one place, every major Strathmore press release that has shaped the story, in reverse chronological order:

Full press release archive: strathmoreplus.com/investors/press-releases. Corporate presentation: February 2026 deck (PDF).

The Closing Argument

The Trump administration has made U.S. uranium a national priority. The producers, Cameco, UEC, Energy Fuels, have already been repriced for it. The explorers, in many cases, have not. Strathmore Plus Uranium (CSE: SUU / OTCQB: SUUFF / FSE: TO3), ticker $SUU, is a Wyoming-focused uranium explorer with three permitted projects, an 85% mineralization hit rate across 294 holes at its flagship Agate property (sitting directly adjacent to ground held by Cameco and UEC), a management team that has built and sold four prior uranium companies, and an explicitly stated next milestone of a maiden NI 43-101 resource estimate. $SUU's market cap is roughly $14 million. The peer-set developers in the same district trade at $700 million to $6.7 billion. Past performance is not a guarantee of future results. Junior uranium investing is speculative and carries the risk of total loss. But if you are looking at the U.S. uranium space right now, you would be hard-pressed to find a cleaner setup or a more under-followed name than $SUU. It deserves the homework.